Looking for lower-cost credit tied to a steady benefit can make sense when rates elsewhere feel high.

INSS consigned loans in Brazil use automatic deductions from monthly benefits to keep costs predictable and approval straightforward for eligible borrowers.

INSS Loan Basics

An INSS loan is a consigned loan linked to Brazil’s Instituto Nacional do Seguro Social benefits.

Installments are deducted directly from the monthly payment, which reduces lender risk and usually results in lower rates than standard personal loans or credit cards.

Similar payroll-deducted products exist worldwide, yet eligibility here depends on holding an INSS benefit in Brazil.

How Automatic Deduction Helps

Automatic deduction removes missed-payment risk and simplifies repayment, which tends to improve approval odds and pricing when compared to unsecured personal loans.

Eligibility: Who Can Apply

Many applicants wonder if their benefit type qualifies, which means confirming status first prevents wasted applications.

- Retirees and pensioners who receive INSS benefits.

- BPC/LOAS social assistance beneficiaries recognized by INSS.

- Public servants or workers in institutions that maintain formal INSS agreements, subject to specific programs.

- A lender may apply different limits, ages, or margins by group, so checking the bank’s matrix in advance avoids surprises at underwriting.

How the INSS Consigned Loan Works

After basic document review and a quick credit check, the bank issues approval and deposits funds in the registered account. Deductions then occur automatically each month until the balance is paid.

Approval

Banks validate identity, benefit status, and available consignment margin, then run a light credit analysis focused on fraud risk and existing consignments.

Funding

Approved amounts are credited to the same account where the benefit lands, typically within one to three business days depending on the bank’s queue.

Repayment

Installments are withheld from the benefit before it reaches the account, so budget planning should reflect the net amount after deduction.

Key Features and Limits

A legal framework caps rates and margins for INSS consignments, and many banks mirror these caps in their internal policies.

| Feature | Standard Practice | Practical Note |

| Interest rate | Regulated ceiling set in Brazil | Usually lower than personal loans due to payroll risk control |

| Term | Up to 84 months | Longer terms reduce installment size but raise total paid interest |

| Consignment margin | 35% of monthly benefit | Typically 30% for loan + 5% reserved for consigned card |

| Processing speed | 24–72 hours post-approval | Times vary by bank and fraud checks |

| Use of funds | No mandated purpose | Treat proceeds as general-purpose credit and plan repayment |

Required Documents

Missing basics stalls approval; in turn, a short checklist keeps the file clean.

- INSS benefit statement (extrato do benefício).

- Government-issued ID (RG or CNH).

- CPF.

- Proof of residence.

- Bank details associated with the benefit deposit.

Digital onboarding through bank apps and the gov.br or Meu INSS platforms is widely available, and e-signature flows have reduced in-branch visits worldwide.

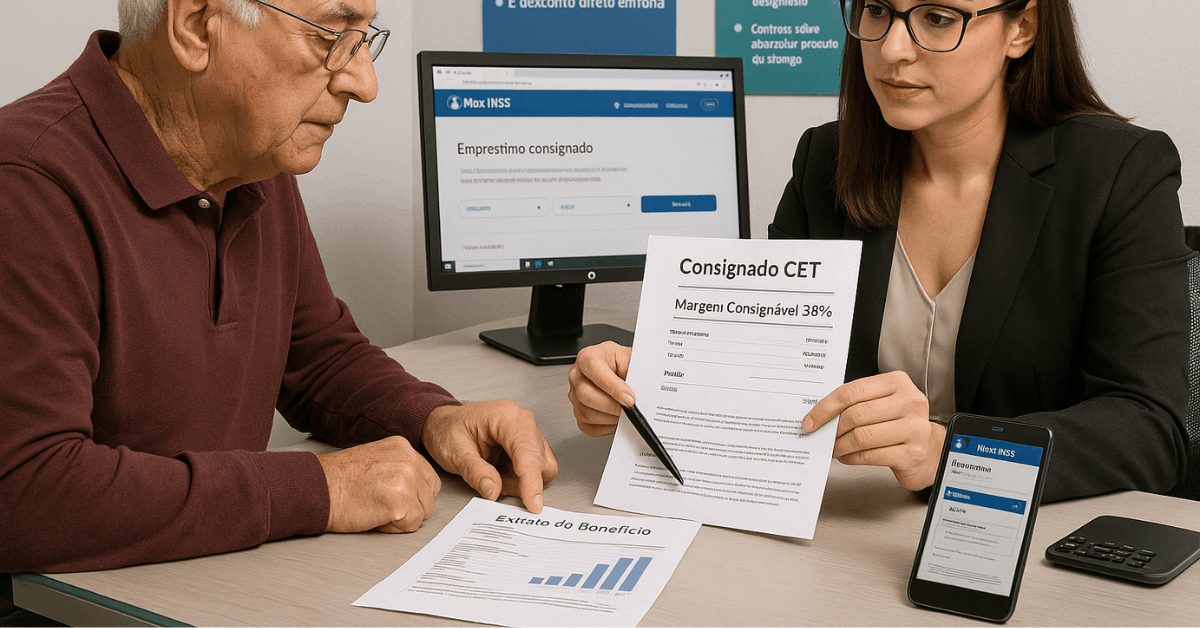

Fees, CET, and Hidden Costs

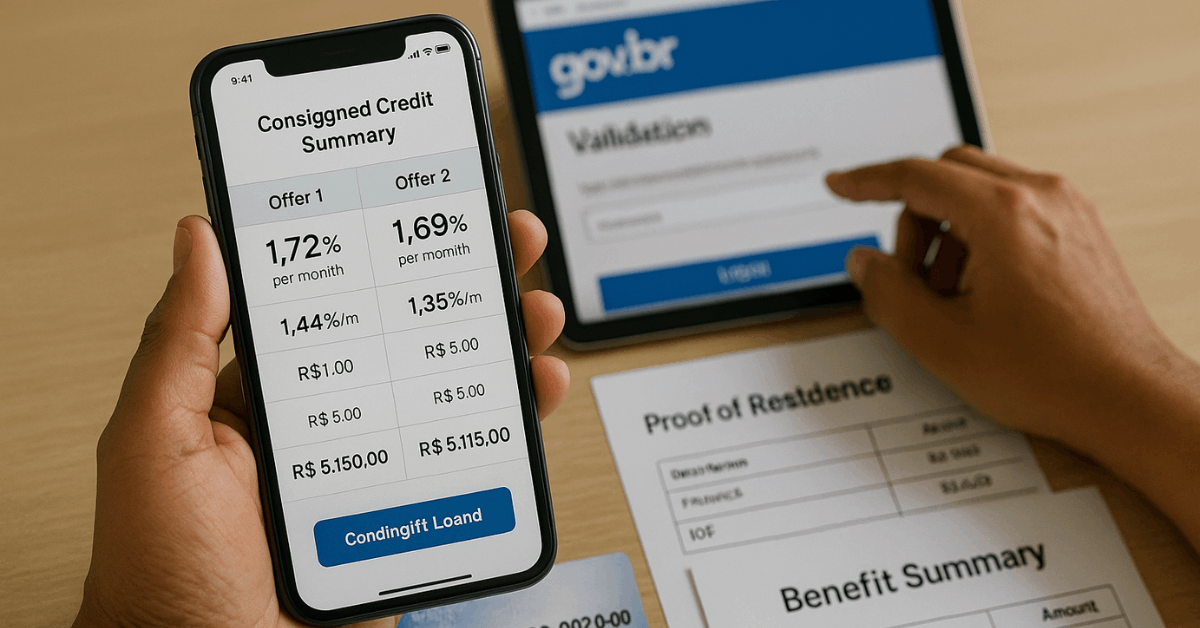

Clear visibility into the CET (Custo Efetivo Total / Total Effective Cost) prevents unpleasant surprises and aligns offers across lenders.

Administrative fees

Some institutions embed small origination or service charges in the financed amount, increasing the CET slightly without changing nominal rates.

Insurance add-ons

Credit life or protection bundles may be optional yet pre-ticked; declining nonessential add-ons lowers total cost when income is tight.

Early payoff rules

Many banks allow advance settlement with interest recalculated on remaining principal; checking payoff math beforehand confirms true savings.

Consigned cards

Consigned credit cards resemble loans due to minimum-payment consignments and separate fee structures; treating them cautiously avoids margin lock-up.

Risks and How to Avoid Them

Retirees and assistance beneficiaries face targeted pressure, therefore a few guardrails curb most problems.

- Over-indebtedness: Keep total consignments below the 35% margin and simulate net benefit after deductions to confirm monthly viability.

- Scams and impersonation: Validate that the lender appears in the Central Bank registry and confirm offers only through official bank channels and the Meu INSS portal.

- Portability abuse: Refuse unsolicited “rate reduction” calls that demand codes or SMS tokens; compare CETs side-by-side before accepting any transfer.

Portability and Refinancing

Moving debt or reborrowing can lower cost or unlock cash, as a result disciplined use matters more than speed.

Portability

Transferring a loan to another authorized bank at a better rate preserves original balance and term while replacing the interest table; requesting a CET for both loans confirms genuine savings.

Refinancing

Recasting the remaining balance into a new contract can release additional funds; however, extending the term too far increases total interest even when the installment falls.

Practical rule

Only accept portability or refinancing when the new CET is lower and the payoff timeline still fits the benefit horizon.

Where to Apply

Channels differ in verification flow and speed, which means choosing the right path shortens funding time.

- Partner bank branches that handle INSS consignments routinely.

- Official online banking platforms operated by major institutions.

- Authorized financial apps listed in government or bank directories.

- Government platforms: Meu INSS app and the gov.br portal for validation and service codes.

Never share passwords or SMS tokens with intermediaries; codes generated in government apps should only be used inside the intended flow.

Common Partner Banks

Provider familiarity helps set expectations on app availability and processing, that way preparation matches each lender’s workflow.

| Institution (Brazil) | Digital Application | Notes |

| Banco do Brasil | Yes | Broad nationwide reach and stable app onboarding |

| Caixa Econômica Federal | Yes | Strong integration with government platforms |

| Itaú / Bradesco / Santander | Yes | Competitive portability offers across regions |

| BMG / PAN | Yes | Specialist consignado operations with fast processing |

| Crefisa | Limited | Branch-heavy processing in select areas |

Institutions regularly update rates, documents, and flows worldwide, so confirming current requirements inside each app or branch remains essential.

Conclusion

INSS consigned loans balance access and control by linking credit to a steady benefit.

Clear rules on rates and margins, along with predictable deductions, make them a practical option for retirees and beneficiaries who want safer borrowing conditions.

Careful review of terms, CET, and repayment impact ensures the loan supports financial stability instead of adding risk.