PicPay operates as a digital wallet and financial services app that lets you pay bills, transfer money, shop online, and request credit directly from your phone.

You can apply, get analyzed, and receive funds without visiting a branch, which makes this option attractive when speed and simplicity matter.

Readers worldwide should note that availability and terms are designed for the Brazilian market; therefore, international users must confirm eligibility and residency rules inside the app.

Who PicPay Loans Are For and How Availability Works

PicPay personal loans and related credit products primarily serve users who hold an active account inside the app and meet basic age and identity requirements.

Offers are personalized according to your credit history, verified data, and in-app behavior, which means two users rarely see the exact same rates or limits.

Eligibility for specific products such as payroll loans or FGTS advances depends on employment type, employer connections, and statutory programs. Key fit indicators:

- You prefer a mobile-first experience and want to avoid in-person paperwork, which makes the end-to-end digital flow a strong match.

- You accept credit analysis tied to your app usage, payment behavior, and credit bureau data, which in turn drives your personalized rate and limit.

- You qualify for specialized products such as FGTS advance or payroll-deducted credit, so that you can exchange lower risk for better pricing.

Types of PicPay Loans You Can Request

Many borrowers get confused choosing among personal, payroll-deducted, or collateralized options; therefore, use the quick breakdown below to match a product to your needs.

Personal Loan

You request unsecured funds for broad purposes such as medical expenses, education costs, or consolidating monthly bills.

Rates and limits depend on credit score, verified income, and account activity, which in turn affects how quickly approval lands and how much you can borrow.

Disbursement happens inside the app, and repayment runs through scheduled installments.

FGTS Advance

You unlock a portion of your FGTS balance before the statutory release date, which helps when you need immediate liquidity while preserving other savings.

Repayment aligns with the FGTS withdrawal schedule, and approval hinges on available balance and regulatory rules.

This option suits workers eligible for the anniversary withdrawal modality who want a predictable deduction from future FGTS releases.

Payroll Loan

You repay through automatic payroll deduction, which typically lowers risk for the lender and produces more favorable interest rates.

Retirees, pensioners, public servants, and eligible employees often qualify when their benefit or employers participates in the program.

Predictable due dates simplify budgeting, and analysis usually completes faster than standard unsecured credit.

Payroll Loan for Employees

You access a payroll-deducted product aimed at private-sector employees under formal contracts, which means installments come out of salary under employer agreements.

Launch timing and partnerships affect availability, and approval depends on your payroll relationship being recognized in PicPay’s network.

Credit Secured by Vehicle

You use a paid-off vehicle as collateral to obtain a larger limit and lower rates compared to an equivalent unsecured loan.

The car remains in your possession during the term, although contract terms allow repossession after sustained delinquency. This route is suitable for borrowers who require larger amounts and can manage the collateral obligations responsibly.

Person-to-Person Loan

You borrow from individuals in a monitored environment inside the app, which reduces reliance on traditional intermediaries.

Pricing and terms vary by supply and demand inside the platform, and participation depends on the product’s current availability and compliance rules.

Interest Rates, Taxes, and the Total Cost

Rates are personalized and vary by product and profile. Personal loans often fall within a monthly range of 1.99% to 5.99%, while payroll-deducted loans can start lower because repayment risk decreases.

Brazilian loans include IOF, the tax on financial operations, which adds a fixed 0.38% plus a daily accrual of approximately 0.0082% over the life of the loan. CET consolidates every cost component, interest, IOF, fees, and insurance where applicable, so you can compare apples to apples across offers.

Typical pricing guide:

- Personal loan: approximately 1.99%–5.99% per month, which reflects your score, income consistency, and recent payment behavior.

- Payroll and consigned loans: often start near 1.30% per month, which generally prices lower due to automatic deduction and lower loss rates.

- FGTS and vehicle-backed loans: commonly priced below equivalent unsecured options, as a result, you exchange specific guarantees for better terms.

IOF and CET in practice

IOF adds 0.38% upfront plus a small daily component around 0.0082%, that way the tax reflects both disbursement and time. CET appears in the offer screen and contract documents, which means you should treat CET as the real annualized picture of cost.

Quick example

R$5,000 over 18 months at a nominal 3.20% per month yields a CET that rises after adding IOF and any administrative fee, which is why you should base comparisons on CET, not headline interest alone.

Limits, Terms, and Installment Flexibility

PicPay commonly offers installment schedules up to thirty-six months, subject to the product type, your analysis result, and regulatory constraints.

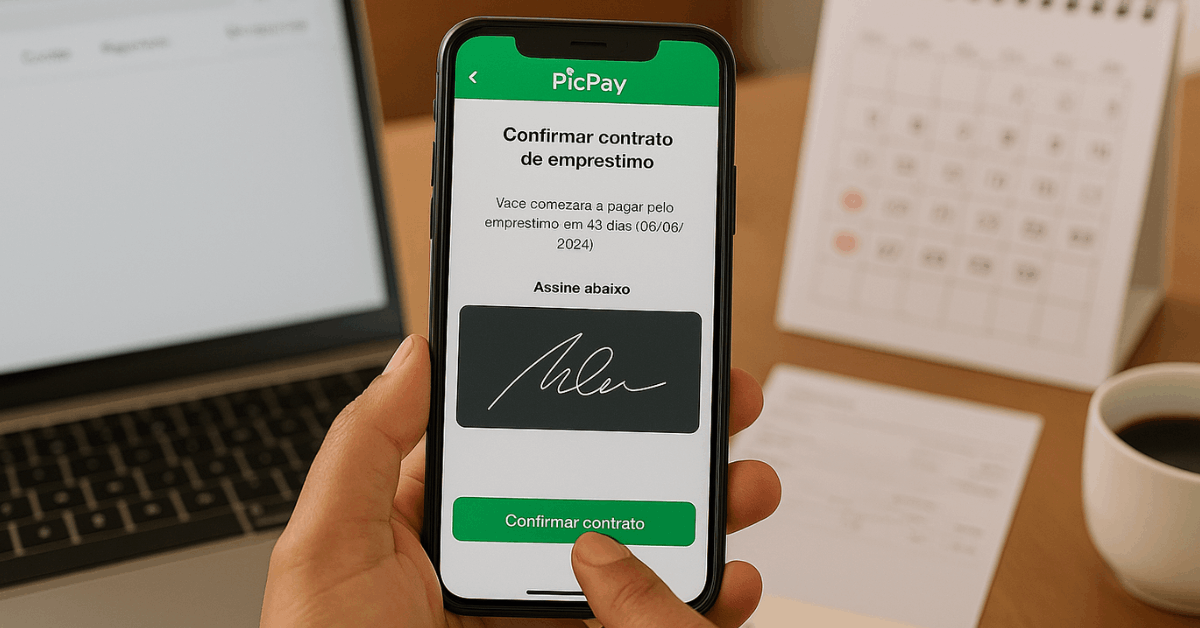

The first installment can be scheduled up to forty-five days after disbursement on select offers, which provides breathing room for cash flow when you need it most. Newer accounts and thin files typically see conservative starting limits that expand as usage, on-time payments, and verified income strengthen the profile.

What influences your limit:

- Verified income, credit score movement, and bill payment history, which together signal capacity and discipline.

- In-app activity, such as paying bills, using Pix transfers, and purchasing via wallet, which in turn builds a stronger internal score.

- The presence of guarantees such as payroll deduction or vehicle collateral allows the lender to reduce risk and raise ceiling amounts.

How to Apply to the PicPay App

Many users overcomplicate the process and miss key steps; therefore, follow a clean sequence that keeps analysis fast and complete.

- Open the PicPay app and sign in to your account, then access Carteira and tap Empréstimos to view available products.

- Choose the loan type that fits your situation, then review the full proposal, including CET and IOF, so the cost is transparent.

- Enter the amount and number of installments that align with your budget, which ensures repayment remains comfortable across months.

- Submit the request and consent to analysis, then upload any requested documents, such as ID or income proof, if prompted.

- Accept the final offer inside the contract screen, and receive funds directly in your PicPay balance after approval completes.

Identity verification and document requests may appear for larger amounts or specific modalities, which means you should keep digital copies ready to avoid delays.

Pre-approved offers sometimes appear in the loan section based on your profile, and accepting those provides a faster path to disbursement.

What PicPay Evaluates During Approval

Guesswork causes frustration during credit analysis; therefore, understand the common factors behind rate and limit decisions.

Core factors in the decision:

- Credit score trends, outstanding debts, and a history of late payments directly influence pricing and acceptance.

- Completeness of profile data, including address, identification, and income details, so that the system can validate your capacity.

- In-app behavior, such as frequency of payments and transfers, acts as a proxy for engagement and reliability.

- Employment type and payroll connectivity, where applicable, which reduces risk and speeds approval for consigned products.

PicPay Versus Traditional Bank Loans

End-to-end mobile flow without branch visits, which removes friction and saves time on documentation. Faster underwriting and instant deposit after approval on eligible offers, so that money arrives when it is actually needed.

Loan management sits next to everyday wallet activity, which simplifies tracking, payment scheduling, and payoff. Preferred clients at traditional banks sometimes access lower headline rates or larger limits, which depend on longstanding relationships.

Complex profiles or substantial amounts can benefit from in-person advisory services, which are particularly helpful during debt consolidation or asset-backed deals.

Security, Regulation, and User Protection

PicPay operates under oversight from the Central Bank of Brazil, which enforces prudential standards and transparency rules for payment institutions and credit operations.

User data is protected and secured under modern encryption practices, and suspicious behavior triggers layered fraud detection to prevent unauthorized actions.

Contract screens display the CET and key terms, allowing you to evaluate costs clearly, and in-app authentication flows minimize the risk of third-party misuse.

Potential Drawbacks and How to Mitigate Them

Any convenient credit channel can carry trade-offs; therefore, prepare for the common downsides and control the impact.

- Higher rates may apply to thin files or lower scores, suggesting that building a history and paying on time before requesting larger amounts is beneficial.

- Lower starting limits appear on newer accounts; that way, you grow into bigger offers after several months of clean usage.

- Regular app activity often improves offers, which means dormant accounts may see fewer or less attractive proposals.

- Vehicle-backed loans introduce collateral risk; therefore, confirm you can meet payments under stress before pledging an asset.

- FGTS advance depends on eligibility and available balance, which limits access to workers under specific statutory rules.

Support and Official Contact Channels

Questions get solved faster when you use the right channel; therefore, keep the following options handy for account and loan issues.

| Purpose | Channel | Availability |

| General Support (SAC) | 0800 025 8000 | Twenty-four hours, seven days a week |

| Ombudsman (Ouvidoria) | 0800 025 2000 | Monday to Friday, 9:00 a.m. to 6:00 p.m. |

| In-App Chat | Ajuda section inside PicPay | During business hours and for ticket follow-ups |

| Data Protection Queries | encarregado@picpay.com | Standard email response times |

| Official Website | picpay.com | Product information and policies |

| Corporate Address | Av. Manuel Bandeira, 291, Condomínio Atlas Office Park, Bloco A, 1º e 2º andares, Vila Leopoldina, São Paulo, SP, CEP 05317-020, Brazil | Mailing and formal notices |

Global readers should rely on the in-app Ajuda area first because channel routing and form requirements stay current there.

If You Saw PicPay Offers Through Aggregators

Some platforms act as marketplaces that connect borrowers to licensed lenders and do not extend credit themselves.

These services may let you start an application or compare offers, which means the contract you sign belongs to the lender selected on that platform, not the aggregator. If you encounter Lendsqr messaging during research, treat it as a facilitator and verify the lender’s identity inside official channels before sharing documents.

Applications initiated outside the PicPay environment should be reviewed carefully since terms, rates, and privacy policies differ from those in-app credit.

FAQs

Short answers reduce back-and-forth during application; therefore, scan these items before you submit a request.

- Can you apply if you are outside Brazil

Availability targets Brazilian residents with local identification; international readers should verify onboarding rules in the app and use local options if residency blocks access. - How old do you need to be

Loan offers generally appear for users between twenty-three and seventy-two years old, which aligns with typical risk and lifecycle policies. - How quickly do funds arrive after approval?

Disbursement often lands instantly in your PicPay balance once you accept the digital contract, although document requests can extend timing. - Can you choose the first payment date

Select offers allow for the first installment to be paid up to forty-five days after disbursement, which helps align cash flow during the first month.

Conclusion

Speed, transparency, and mobile convenience make PicPay a strong candidate when you need digital credit delivered fast and managed in one place.

You get a choice of products, unsecured personal loans, payroll-deducted options, FGTS advances, vehicle-backed credit, and person-to-person lending, plus flexible terms that can reach thirty-six months and initial payments that sometimes start after forty-five days.

Careful budgeting, on-time repayment, and steady app usage build a profile that earns higher limits and better terms over time, which turns this channel into a reliable part of your financial toolkit worldwide.

Disclaimer

Information here serves educational purposes and does not replace professional advice.

Rates, availability, and eligibility change according to your credit analysis and PicPay’s internal policies; therefore, review your contract carefully and consult a qualified advisor when needed.